The Indian rupee recently registered a sharp devaluation with respect to the dollar after remaining stable for over two years or so. What explains such a phenomenon? What are the implications? This article aims to address these issues by discussing India’s exchange rate policy and highlighting a few structural constraints in the Indian economy in the recent period.

Exchange rate regimes

The nominal exchange rate is the price of buying one unit of foreign currency in terms of domestic currency. The way in which the nominal exchange rate changes depends both on the demand-supply conditions of the foreign exchange market and the exchange rate policy of the central bank.

The real exchange rate is the relative price of foreign goods in terms of the domestic currency with respect to the prices of the domestic goods. It describes how cheap or costly domestic goods are concerning the foreign goods.

The demand and supply conditions of the foreign exchange market depend on the flows of the current account and capital account. The demand for foreign currency would rise if the sum of net current account and capital account flows falls, whereas the supply of foreign currency would rise if the sum increases. The net current account flows are largely influenced by the net exports, whereas net capital account flows are influenced by the net flows of foreign investments. The lower the net exports and greater the capital outflow, the greater would be demand for foreign currency and vice-versa.

Depending on how the central bank responds to the demand and supply conditions in the foreign exchange market, there can be broadly three kinds of exchange rate policy frameworks — fixed exchange rate, floating exchange rate, and managed-floating exchange rate regimes.

In the fixed exchange rate regime, the central bank responds to the higher demand for foreign currency entirely by selling (decumulating) foreign exchange reserves (and vice versa), while keeping the nominal exchange rate fixed at a predetermined level.

In the floating exchange rate regime, the central bank responds to higher demand of foreign currency entirely by devaluing the domestic foreign currency (making foreign currency costlier in terms of domestic currency) and vice versa, while keeping the level of foreign exchange reserves unchanged.

In the managed-floating exchange rate regime, the central bank responds to higher demand for foreign currency both by selling foreign currency as well as devaluing the domestic foreign currency.

Barring a few brief episodes, India has largely pursued a managed-float exchange rate regime in the last three decades. The last decade has been characterised by the Reserve Bank of India (RBI) pursuing a particular variant of managed-float exchange rate regime, where its response under excess demand conditions in the foreign exchange market has been qualitatively different from excess supply conditions. Under excess demand conditions in the foreign exchange market, the RBI has simultaneously devalued the domestic currency and decumulated its foreign exchange reserves. However, under excess supply conditions, the RBI accumulated foreign exchange reserves while largely resisting appreciation of the nominal exchange rate to avoid appreciation of the real exchange rate or the worsening of export competitiveness. By implication, while episodes of net capital outflow were associated with depreciation of the nominal exchange rate, the episodes of net capital inflow did not involve appreciation of the exchange rate to the same extent. This asymmetry in the behaviour of the nominal exchange rate led to an overall devaluation of the rupee throughout the 2010s decade as reflected in Figure 1.

In the post-COVID period, particularly between the latter half of 2022 and November 2024, the RBI momentarily shifted its policy stance to a regime that closely resembles the fixed exchange rate regime. This is reflected by the flat segment of the dollar exchange rate in Figure 1 during the relevant period. Deterioration of the current account deficit and capital outflow during this period were met by selling foreign exchange reserves while holding the nominal exchange rate more or less at the same level. The sharp devaluation of the rupee in the last month or so hints towards RBI returning to its earlier regime of the managed-float exchange rate that it followed during the 2010s. Responding to greater capital outflow and a rise in imports amid higher crude oil prices, the RBI allowed the rupee to depreciate with the objective of putting less strain on the foreign exchange reserves.

Implications of devaluation

Depreciation of the nominal exchange rate can have at least two macroeconomic implications — positive and adverse. The first route involves the real exchange rate channel, whereas the second route involves the prices of domestic goods.

Cheapening domestic goods opens up the possibility of increasing net exports. For example, if the nominal dollar exchange rate is ₹85, the dollar price of foreign goods is $100 and the rupee price of domestic goods is ₹1,000, then the prices of foreign goods in terms of the domestic currency would be ₹850 and the real exchange rate would be 0.85.

First, a depreciation in the nominal exchange rate can positively influence net exports and output if two conditions hold simultaneously: (i) the net exports respond positively to the real exchange rate and (ii) depreciation in the nominal exchange rate is associated with depreciation in the real exchange rate. A rise in domestic prices at a given nominal exchange rate would lead to an appreciation of the real exchange rate by making domestic goods costlier, whereas a depreciation of the nominal exchange rate at unchanged domestic prices would lead to a depreciation of the real exchange rate by making domestic goods cheaper with respect to foreign goods.

Second, a depreciation in the nominal exchange rate can increase domestic prices by increasing the variable cost of firms and putting a greater squeeze on real income. In oligopolistic markets, firms typically set their prices by setting a markup over their variable cost. Since the variable cost of firms typically includes the cost of imported war materials, nominal exchange rate depreciation would increase the variable cost of firms by increasing their effective cost of imported raw materials. The consequent rise in variable costs leads to higher prices when the firms pass on the burden of higher raw material costs to the final consumers.

The central constraint that emerged in the Indian economy since the latter half of the 2010s, however, was that the condition for the positive effect of nominal exchange rate depreciation ceased to hold.

The recent constraint

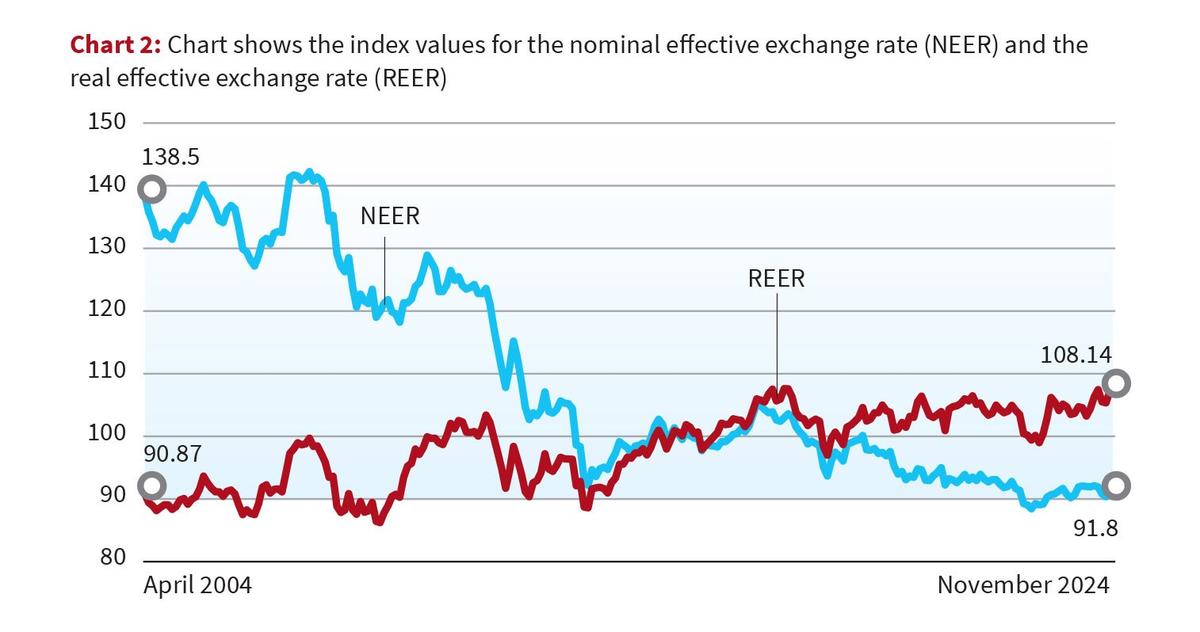

The period since the mid-2010s, particularly 2019 has been characterised by the growing divergence between the nominal and the real exchange rate. Figure 2 shows this divergence by plotting the trend in the nominal effective exchange rate (NEER) and the real effective exchange rate (REER). These indices reflect the weighted average exchange rate of India with respect to its multiple trade partners. The way in which these indices are defined, any increase or positive change of these indicators implies appreciation, and any decrease or negative change implies depreciation.

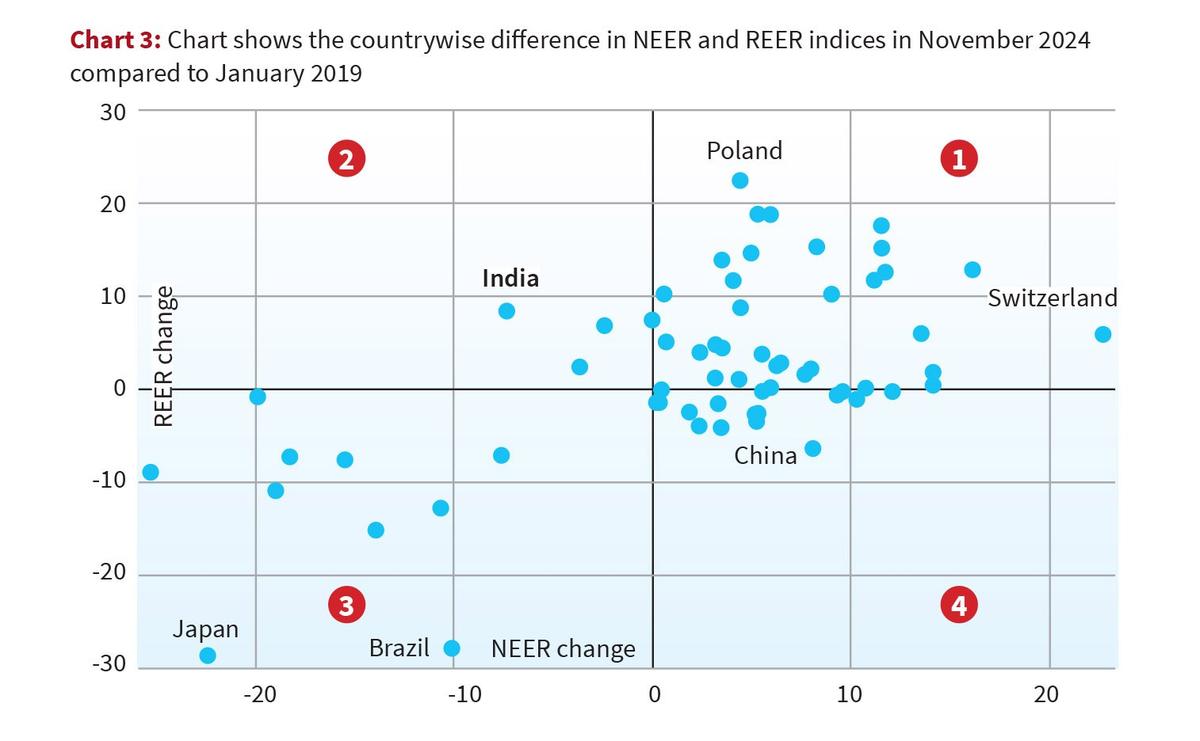

After moving in the same direction till the mid-2010s, they started moving in opposite directions with the real exchange rate registering an appreciation despite a depreciation in the nominal exchange rate. Such a phenomenon distinguishes India from the bulk of the other countries. Figure 3 shows this by depicting the exchange rate movements of 62 countries using data from the Bank of International Settlements (BIS). The horizontal and the vertical axis respectively measure the change in the indices of NEER and REER between January 2019 and November 2024. The vertical zero-line marks no change in the NEER, while the horizontal zero-line marks no change in the REER.

Depending on how both NEER and REER changed during this period, Figure 3 can be divided into four boxes or categories. Category 1 includes countries where both nominal and real exchange rates registered appreciation. Category 2 includes countries where the real exchange rate appreciated despite the depreciation in the nominal exchange rate. Category 3 countries are those which registered depreciation in both nominal and real exchange rates. Category 4 countries are those which registered depreciation in the real exchange rate despite the appreciation in the nominal exchange rate.

The figure shows at least two important features of the global economy during this period. First, the majority of countries have been located in categories 1 and 3, indicating that the nominal and real exchange rates have moved in the same direction for most countries. Second, India parted company with most countries since 2019, as it is located in category 2.

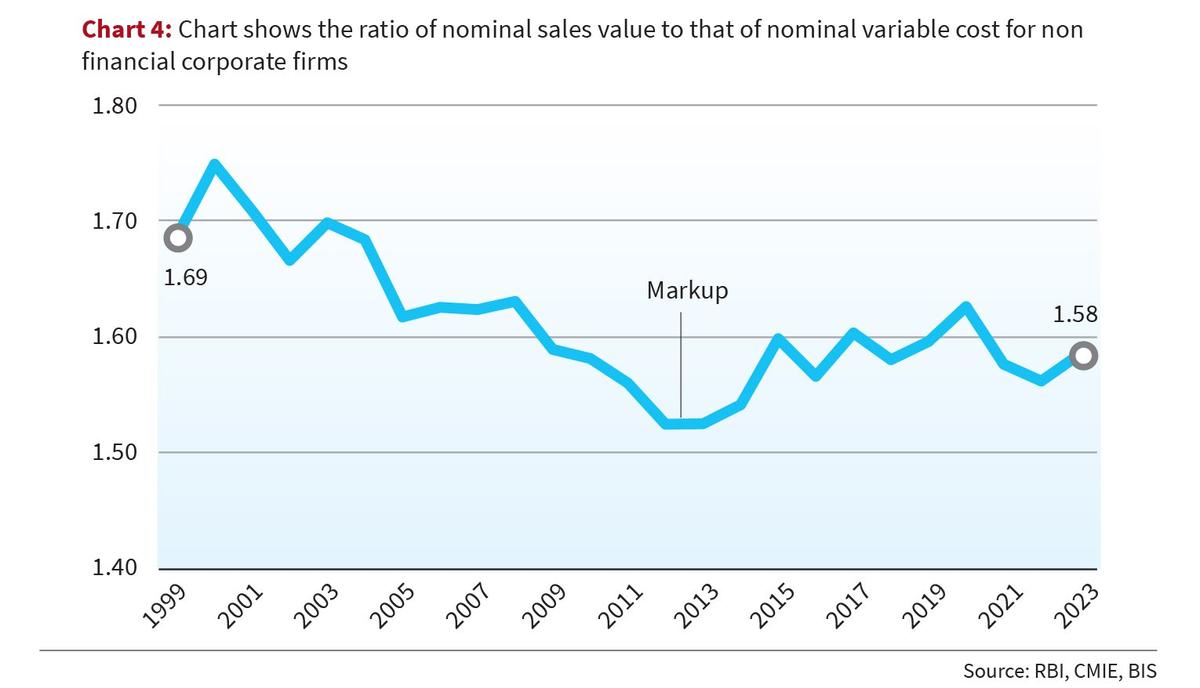

Such appreciation of the real exchange rate in India despite a depreciation of the nominal exchange rate indicates that the latter has been associated with counteracting rise in domestic prices. One explanation for such a rise in domestic prices can be located in the recent increase in the markup of non-financial firms as shown in Figure 4.

The markup can be estimated as the ratio between the output price and the variable cost per unit of output or the ratio between the nominal value of sales and the total variable cost. Figure 4 shows the trend in the markup for 1908 sample firms in the Centre for Monitoring Indian Economy (CMIE) Prowess database which has provided information on their variable cost in all the years in the sample period. The variable costs in this estimation include the expenses on raw materials, packaging, power, and fuel, compensation to employees, indirect taxes, distribution, and outsourcing. After registering a decline till the mid-2010s, the markup reversed its trend and started rising. Since prices are formed by a markup over variable costs, any rise in markup would push up domestic prices at any given level of variable costs and nominal exchange rate.

The policy question

While the weakening of the rupee puts pressure on the prices, the delinking of the real exchange rate from the nominal exchange rate has posed additional constraints on the recovery of net exports and the balance of payments adjustment mechanism. This leads to the larger questions for the exchange rate policy — should India return to the earlier strategy of the 2010s, or does it require a new and explicit exchange rate policy framework? What should the exchange rate policy aim to achieve?

The response of the RBI in the post-COVID period has appeared somewhat arbitrary, as it has frequently shuffled its policy stance without providing adequate explanation. The recent challenges bring forth the need to address these questions in a more systematic way.

Zico Dasgupta teaches economics at Azim Premji University

Published – January 16, 2025 10:37 pm IST